2.

Please provide your organization’s feedback on the Phase 1 proposal to institute a bid and price floor in the CRR auction, as described on slides 11–28 of the CAISO presentation and in Section 4.3 of the straw proposal.

Please include any comments on which of the options shown on slide 28, or other floor levels not presented, is most appropriate and why.

BAMx believes that its proposal to limit auction participation to those entities that have historically used the CAISO’s physical transmission system would be simpler to implement than the bid and price floor in the straw proposal. The CAISO and DMM already possess the information necessary to apply such limits, and similar limits already placed on allocation CRRs can guide the development of participant limitations for auction CRRs. This approach directly addresses the CRR working group Problem Statements 1, 2, and 5, related to auction revenue adequacy, participant contribution to fair allocation of congestion revenues, and addressing evolving hedging needs for users of the transmission system.[1]

Another viable short-term alternative raised in the stakeholder process might be to allocate auction-driven revenue shortfalls exclusively to the entities that do not use physical transmission in the CAISO and therefore are not using CRRs for FERC’s anticipated purposes: to hedge physical energy or to return congestion revenue to transmission ratepayers.

Though BAMx considers the bid-price proposal to be a less direct measure than our proposal to limit auction participation and could divert attention from more effective solutions, we would like to offer our analysis of the bid-price bounds proposed by the CAISO and discuss some suggestions regarding the structure of the price bounds proposal.

Symmetrical Price Bounds

BAMx is concerned that the lack of symmetry in positive and negative price bounds could provide an opportunity for parties to thwart the intent of the bounds or create unintended consequences. Specifically, the CAISO proposes a -$0.10/MWh ceiling for negatively priced CRRs but floors of $0.25–$1.00/MWh for positively priced on-peak CRRs.[2] This asymmetry could create incentives for auction participants to use counterflow bids strategically to drive clearing prices below the bid floor on prevailing-flow paths, effectively circumventing the floor on positive-value CRRs. Perhaps the proposed price floor would effectively override such efforts, as suggested during the MSC discussion on June 11, 2026. BAMx recommends that the CAISO evaluate whether symmetric positive and negative bounds would better prevent such outcomes.

Backstop Mechanism

Because the root of revenue insufficiency seems to be both the low price and excessive quantity of CRRs released by the CAISO in the CRR auction, the bid-price floor construct should be designed only to restrict the CAISO from releasing too many CRRs at too low of a price. The bid-price floor should not apply to CRRs sold by entities that received them in the allocation or auction processes. CAISO CRR staff indicated during the June 11, 2026, MSC meeting that it should be feasible to not apply the bid-price floor to those transactions. In an efficient market, entities that already hold revenue rights should be able to sell them for whatever price they are willing to accept for those rights. Limiting entities’ ability to sell their own CRRs for any price they are willing to accept risks bringing the liquidity concerns raised by other entities to fruition.

On that note, based on the pricing analysis discussed below, BAMx does not believe that any of the pricing groups proposed by the CAISO would meaningfully limit entities’ ability to sell their CRRs at auction. There is substantial auction activity remaining at levels above the bid-price limits proposed by the CAISO, and financial and marketing entities are still major participants at those levels. As demonstrated below, the limits proposed by the CAISO will put limits on the ability to gain windfall profits from cheap CRRs that consistently yield positive notional values while preserving LSEs ability to sell allocation CRRs to rebalance their portfolios.

Pricing Analysis

If CAISO chooses to move forward with the bid and price floor structure from the straw proposal, BAMx recommends setting the auction bid and price floor at group 3, or $1.00/MWh for on-peak CRRs and $0.25/MWh for off-peak CRRs. Based on our analysis of 2024 CRR auction clearing data, and a variety of bid and price floors, including those proposed by the CAISO, we believe that the third group of prices proposed by the CAISO is the optimal level. Table 1 shows the bid-price floors tested by BAMx in the following analysis.

Table 1: Bid-Price Groups for CRR Buy Transactions

|

Group

|

On-Peak ($/MWh)

|

Off-Peak ($/MWh)

|

|

1

|

$0.25

|

$0.05

|

|

2

|

$0.50

|

$0.10

|

|

3

|

$1.00

|

$0.25

|

|

4

|

$1.25

|

$0.35

|

|

5

|

$1.50

|

$0.50

|

|

Negative

|

-$0.10

|

-$0.10

|

BAMx used the entity-level CRR auction clearing data from our 2025 CRR analysis[3] and assigned the CAISO Department of Market Monitoring’s entity-type designations to the entities associated with each CRR observation. We then converted the price per MW to price per MWh by dividing the CRR buy MW quantity by the hours in each monthly time-of-use period. Next, we assigned a variable to each CRR observation indicating whether it would have cleared at each of the various pricing bands shown in Table 1.[4]

BAMx aggregated the 2024 CRR auction results to the monthly TOU level and determined the number of observations (N), the total buy MW, the total buy cost, and the notional value before clawbacks. Relative to the baseline, we calculated the proportion of CRR observations, buy MW, buy cost, and notional value that would have cleared or not cleared under each price group.

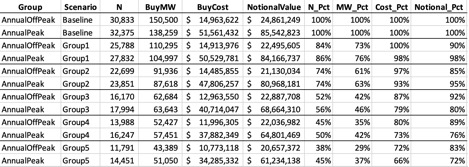

Table 2: Annual 2024 CRRs "Cleared" by TOU Bid-Price Group

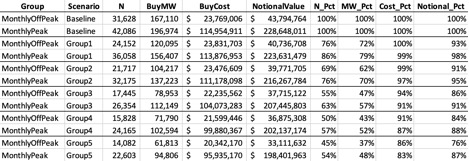

Table 3: Monthly 2024 CRRs "Cleared" by TOU and Bid-Price Group

Table 2 and Table 3 show these summaries at the annual and monthly time-of-use level, respectively, by bid-price group. In each of these tables, the “_Pct” columns show the proportion of CRR observations, buy MW, buy cost, and notional value that clear for each price group. A substantial volume of CRRs exists below each of the three bid-price groups proposed by the CAISO. Under groups 1 and 2, around 20% - 30% of transactions and volume are excluded but roughly 97% - 99% of the total auction buy cost (representing perceived value to the auction buyers) is preserved. Groups 1 and 2 both represent a negligible share of the cost paid for auction CRRs but a meaningful share of the notional value paid out to CRR holders. Group 3 seems to strike something of a balance, where the reduction to costs paid is broadly similar to the reduction in notional value (i.e., while there is an approximately 40% reduction in transactions and MW volume, there is an approximately 10% reduction in buy cost and notional value realized).

BAMx estimates that CRRs excluded under Group 3 contributed a net excess of approximately $20.9 million in payouts over auction revenue in 2024, representing roughly 18% of the CAISO's reported average annual shortfall of $114 million. This confirms that these low-price CRRs are not merely low-value, rather they are net contributors to revenue inadequacy. Relative to the low buy cost value, the contribution to revenue inadequacy is much more significant than the contribution from higher valued auction CRRs. The analysis shows that the Group 3 bid-price floors result in 40% - 50% of the auction MW being removed from the auction while preserving 85% of overall buy cost and notional value. Moving past group 3, the improvement to revenue adequacy diminishes.

This demonstrates that a substantial number of CRRs are being sold for prices that are systematically lower than their realized value and that a remedy is warranted. Transmission-use-based participation restrictions, a method to allocate underfunding to the entities that are driving the underfunding, or bid-price floor are all short-term modifications to the CRR auction process that might suit this need.

The impact of these changes is not uniform across entity types. It appears entities that have no evident use of CAISO’s transmission system in 2024 EQR data have consistently extracted value from CAISO transmission ratepayers by taking speculative positions on these cheap CRRs with notional values that regularly exceed their buy cost.

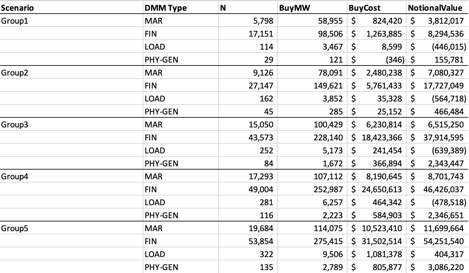

Table 4: Aggregate 2024 Baseline CRRs by Entity Type

Table 4 above shows the baseline of CRRs that cleared in the 2024 auction. What is immediately evident from the baseline is that financial entities, who typically do not actually use the physical transmission system in CAISO[5], receive disproportionate notional value from their participation in the 2024 CRR auctions compared to their spending on auction CRRs. This arises from financial entities consistently purchasing low or negatively priced CRRs that subsequently realize significantly higher notional value. This pattern is consistent with speculative arbitrage, not physical hedging.

Table 5: Aggregate 2024 "Not-Cleared" CRRs by Entity Type and Bid-Price Group

This pattern is also evident in the CRRs that would be excluded under each of the bid-price groups. Table 5 shows the CRRs that would not clear with of the five bid-price groups, aggregated by the entity types defined by DMM. The second row (Group1-FIN) shows that there were approximately 17,150 source-sink pairs representing 98,500 MW of capacity, $1,264,000 total cost, and $8,295,000 notional value purchased by financial entities in the 2024 auction that would be excluded by the group 1 bid-price bounds. This represents an approximately $7 million contribution to revenue inadequacy in the 2024 auction from entities with no identifiable use of the physical CAISO transmission system. This grows to approximately $19 million with the group 3 price bounds.

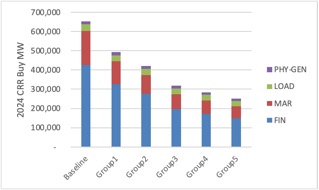

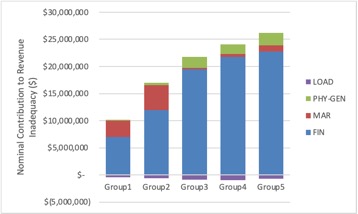

Figure 1: "Cleared" CRR Buy MW by Entity Type and Group in 2024

Figure 1 shows the MW that “clear” under each of the price groups and demonstrate once again that most of the combined annual and monthly auction CRRs that do not clear under these price bounds are ones held by financial entities that do not have identifiable use of the CAISO transmission system in 2024 EQR data. Volume purchased by physical generators and load serving entities shows little change under any of the bid-price groups, because these entities are paying for hedges for their load or generation and, in the case of investor-owned utility LSEs, are prohibited from engaging in speculative activity.

The data in Table 5 and Figure 1 also demonstrate that the CRRs that would be eliminated under the Group 1-3 bid-price floors are not serving the purposes of financial transmission rights identified by FERC. They extract value from transmission ratepayers rather than returning congestion revenue to transmission ratepayers.

By comparing the price paid for CRRs to the notional value of the CRR, BAMx estimated the contribution of each entity’s source-sink pairs on revenue adequacy. We then collected the set of CRRs that would be excluded under each of the five bid-price groupings and assessed the extent that those CRRs contribute to underfunding from the buy-side of the 2024 CRR auction.

Figure 2: Contribution to Revenue Inadequacy by Type and Bid-Price Group in 2024

Figure 2 demonstrates that eliminating these cheap, speculative CRRs will yield improvements to revenue adequacy that are larger than the corresponding reduction in CRR auction buy costs. Purchases of these low-cost CRRs contribute a substantial and disproportionate amount to revenue inadequacy in the CRR auction. Interestingly, at group 3, marketer entities see little net impact because roughly half of the CRRs purchased by marketer entities in group 3 ended up settling for negative notional values.

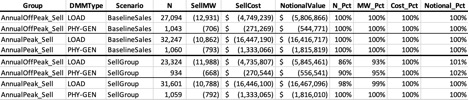

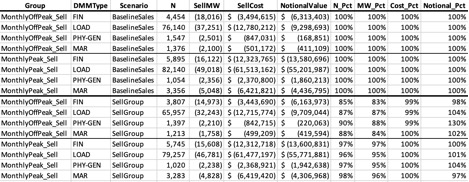

BAMx also evaluated the potential impact on sell-side outcomes from the -$0.10 proposed price floor for negatively priced transactions. We found that most of the impact is limited to sales of off-peak CRRs with fairly muted impact to sales of on-peak CRRs. Ninety-eight percent of annual peak CRR sales remain, along with 86% of annual off-peak sales, 96% of monthly peak sales, and 87% of off-peak CRR sales.

Table 6: Sales of Annual CRRs by Bid-Price and Type for 2024

Table 7: Sales of Monthly CRRs by Bid-Price and Type for 2024

Table 6 and Table 7 show the fairly limited impact that the negative price bound has on sales of previously allocated or purchased CRRs, particularly to on-peak CRRs. It’s also apparent from these tables that many of the low-priced CRRs being sold at auction end up yielding positive notional value. This suggests that entities that are selling these low-priced CRRs would be financially better off if they kept them instead. That pattern is different for financial entities selling monthly CRRs, who appear to be selling CRRs that will ultimately reduce the total rents that they are able to extract from CAISO transmission ratepayers. This pattern is once again consistent with entities that are using CRRs other than as a hedge for physical transmission.

Our analysis reveals a fundamental flaw in the current CRR auction process. CRR volume is being released into the CRR auction at prices that are consistently lower than their notional values. This suggests that the CAISO CRR auction is systematically undervaluing the CRRs that are being released into the auction, and it is releasing substantially more volume than is justified by actual hedging needs. This results in a systematic transfer of value from transmission ratepayers to the entities that are purchasing those undervalued CRRs. This finding is inconsistent with assertions that low-price CRR transactions do not disproportionately contribute to auction revenue shortfalls. While excess payouts may not be concentrated in a single price category on a per-MWh basis, they are disproportionately concentrated in volume at the lowest price levels. This is exactly the pattern a bid and price floor is designed to address.

Based on this analysis, BAMx suggests that if a bid-price floor is ultimately adopted by CAISO, the bounds should be set near those from group 3: $1.00/MWh for on-peak CRR purchases and $0.25/MWh for off-peak CRR prices. Given concerns expressed by stakeholders about unintended consequences, and the relatively small impact on auction inefficiency and revenue adequacy of the bid-price floor, BAMx recommends not pursuing the bid-price floor approach and instead pivoting immediately to Phase 2 to focus on more effective solutions to addressing the CRR auction problems. While potentially useful as an incremental measure, the bid-price floor mechanism does not address the fundamental structural issue that the CAISO releases excessive CRR volume at prices that systematically undervalue congestion rents. BAMx's preferred reforms for Phase 2 remain (1) participation limitations aligned with historical transmission use, and (2) continued development of the willing seller design. BAMx urges the CAISO to prioritize these structural reforms in Phase 2 regardless of the outcome of Phase 1.

[1] CAISO Straw Proposal, June 1, 2026, p. 6.

[2] CAISO Straw Proposal, June 1, 2026, p. 18.

[3] Bay Area Municipal Transmission Group (BAMx), “Analysis of CRR Auction Participation,” May 12, 2025. https://stakeholdercenter.caiso.com/InitiativeDocuments/Presentation-BAMX-Congestion-Revenue-Rights-Enhancements-May-12-2025.pdf

[4] In principle, auction participants would change their behavior in response to these bid-price floors. This analysis is unable to capture that nuance without re-running a simulated CRR auction for 2024.

[5] Bay Area Municipal Transmission Group (BAMx), “Analysis of CRR Auction Participation,” May 12, 2025. https://stakeholdercenter.caiso.com/InitiativeDocuments/Presentation-BAMX-Congestion-Revenue-Rights-Enhancements-May-12-2025.pdf